What’s Next for NVIDIA? A Big Earnings Call, A Big Question Mark

NVIDIA has dominated the AI space for the past two years, driving massive stock gains and securing its place as the undisputed leader in AI computing.

NVIDIA has earnings coming up this Wednesday (February 26, 2025), investors are asking a critical question: Can NVIDIA push even higher, or is the stock finally due for a pullback?

This earnings report will be a major test for the AI market, determining whether NVIDIA can keep up its explosive growth or if the competition is finally catching up.

Where NVIDIA Stands Right Now

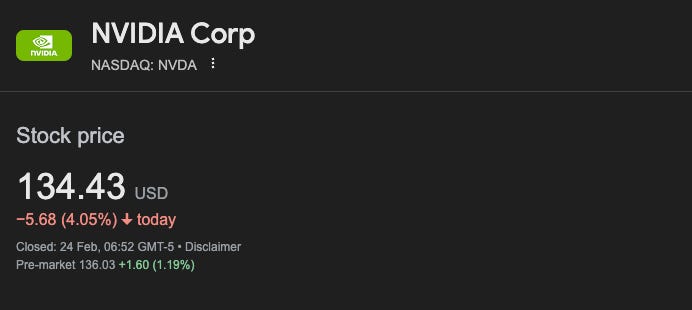

As of February 24, 2025, NVIDIA's stock is trading at $134.43, down 4.05 percent in the past 24 hours. While that may not seem like a drastic drop, it stands out when you consider the company’s massive run over the past two years.

In 2023, NVIDIA soared by 239 percent. The momentum carried into 2024, with another 172 percent gain. But in 2025, things have been different. So far, the stock has remained flat to slightly down, a stark contrast to its previous parabolic moves.

This cooldown is not just a breather after two years of explosive growth. It reflects a shift in market dynamics, where competition is intensifying, valuations are stretched, and questions about sustained AI demand are becoming more relevant.

A High Bar to Clear

Wall Street analysts expect NVIDIA to report $37.5 billion in revenue for Q4 FY25, a staggering 70.68 percent increase from $21.9 billion in Q4 FY24.

To put that into perspective, Apple pulled in around $90 billion in revenue during Q4 2024, while Microsoft reported $62 billion. For NVIDIA, a company that was generating just $5 billion per quarter in 2020, reaching this level of revenue in such a short time is unprecedented in tech history.

The surge is almost entirely driven by AI-related demand, as companies scramble to secure NVIDIA’s cutting-edge GPUs for their AI models and data centers. But the market has already priced in this growth to some extent.

Now, the real question is not just whether NVIDIA meets or beats expectations, but what happens next. Investors will be paying close attention to guidance, looking for any signals about how sustainable this level of demand really is.

Competition is Closing In

For nearly two years, NVIDIA has been the dominant force in AI chips, with its H100 and A100 GPUs powering the majority of AI models on the market. Any company training or running large AI models has almost certainly been relying on NVIDIA’s hardware.

But the AI landscape is shifting, and competition is becoming more serious.

A Chinese startup, DeepSeek, has entered the scene with AI models that are reportedly cheaper than those from OpenAI and Google DeepMind. While this does not directly threaten NVIDIA’s GPU sales, it introduces a shift in market dynamics. If companies can train and run AI models more efficiently with fewer GPUs, it could slow down the rapid pace of AI hardware purchases, which has been a key driver of NVIDIA’s revenue growth.

Meanwhile, big tech firms like Google, Amazon, and Microsoft—historically some of NVIDIA’s biggest customers—are investing heavily in proprietary AI hardware to cut down their reliance on NVIDIA.

Google is pushing its TPUs (Tensor Processing Units) deeper into AI training and inference.

Amazon has Trainium, a custom AI accelerator for its AWS cloud services. Microsoft is developing Athena, an in-house AI chip aimed at reducing costs and improving efficiency.

These companies have been buying tens of billions of dollars worth of NVIDIA GPUs, but as their own hardware matures, they could begin reducing those purchases. At the same time, AMD and Intel are ramping up their AI chip offerings.

AMD’s MI300X is being marketed as a lower-cost alternative to NVIDIA’s H100, targeting companies looking to cut expenses while still accessing high-performance AI computing.

Intel’s Gaudi 3 AI accelerator is another cost-efficient option gaining traction. While NVIDIA still holds the performance edge, competitors are getting closer—and if pricing becomes a key factor, some buyers may start shifting away from NVIDIA.

NVIDIA’s answer to this increasing competition is Blackwell, its next-generation GPU architecture, which is expected to deliver a huge performance jump over the current Hopper-based H100. But there are already signs of potential issues.

NVIDIA relies on TSMC’s 3nm process, which is in high demand from other chipmakers like Apple, AMD, and Qualcomm. Production constraints could limit Blackwell’s availability in its early rollout.

Some analysts believe that the initial supply of Blackwell GPUs will be lower than expected, meaning customers may face delays in acquiring the new hardware.

Pricing will be a major factor—with H100s already selling for over $30,000 per unit, if Blackwell pushes prices even higher, smaller AI startups may be forced to look for alternatives like AMD or Intel.

If NVIDIA can deliver Blackwell on time and at scale, it could reinforce its AI dominance for another product cycle. But if delays or pricing concerns emerge, it could open the door for competitors to take market share.

Where Does NVIDIA’s Stock Go?

NVIDIA’s stock has been moving inside a descending channel since mid-December, meaning sellers have controlled the trend for the past two months.

Key Levels to Watch

Support: $130, $113, and $102 – These levels will be critical if NVIDIA drops after earnings.

Resistance: $153, then $174 – If NVIDIA beats earnings and raises guidance, a breakout above $153 could send the stock higher.

A bearish engulfing pattern recently appeared, signaling a possible move lower. However, earnings reports often override technical setups, meaning anything is possible in the short term.

Bull vs. Bear: What Happens on Wednesday?

Bullish Case (Stock Moves Higher)

NVIDIA beats revenue expectations and guides higher for 2025.

AI demand continues accelerating, with NVIDIA maintaining its dominance in GPU sales.

No major Blackwell chip delays, allowing NVIDIA to maintain its competitive edge.

Bearish Case (Stock Pulls Back)

NVIDIA misses earnings or lowers guidance, triggering a sell-off.

AI demand shows signs of slowing, with companies scaling back GPU orders.

Competition from Google, AMD, and Intel starts eating into NVIDIA’s market share.

This is the most important earnings report for NVIDIA in years. If the numbers are strong and guidance is positive, NVIDIA could reignite its stock rally. But if there are any cracks in the AI growth story, it could send the stock lower.

Final Thoughts

NVIDIA’s insane growth over the past two years has made it the undisputed leader in AI computing, but 2025 is shaping up to be a much tougher year, let alone the years to come…

The stock is no longer running higher every week like in 2023 and 2024. Competition is intensifying, with big players designing their own AI chips. Investors need to see NVIDIA prove that the AI boom still has legs.

This week’s earnings report will set the tone for the rest of the year. If NVIDIA exceeds expectations, we could see the stock push toward new highs. But if guidance disappoints, this could be the beginning of a long-overdue pullback.

Either way, this is the biggest earnings event of the week, and all eyes are on NVIDIA.

Given my analysis, I estimate the price after earnings to stabilise between $150-$170.

Full disclosure I am bullish on NVIDIA, but I try to be as objective as possible in my analysis, My estimated price range after earnings is based on assuming NVIDIA will outperform, and of course results may differ, we have seen occasions where. with good results it went the opposite direction.